Motorbike insurance in Thailand is compulsory if you’re planning to ride around and explore this beautiful tropical country on your own. You could buy a used car or rent a cab, but if you want to immerse yourself in the local culture, and take your time sightseeing, then a motorbike is easily the best way to get around. If you’re traveling light or staying in a place like Phuket where so many tourist spots and unique cultural experiences are packed together, then a bike is perfect for you.

If you’ve just landed in Thailand for a long holiday or traveled there for work, a bike will be much cheaper than investing in a car to get around the place. However, accidents can and do happen, especially if you’re staying in a city like Bangkok. There are a lot of vehicles suddenly changing lanes, and many do not even signal. If you’re unfortunate enough to get into a traffic collision, you’re gonna need some motorbike insurance. So let’s find out everything we can about motorbike insurance in Thailand.

The Two Types of Motorbike Insurance You Can Buy in Thailand

There are two types of motorcycle insurance you can get in Thailand. First, there is compulsory motorbike insurance with its basic insurance coverage that you receive when you purchase and register your bike. There’s also voluntary motorcycle insurance you can purchase from a private insurance company which will provide much more comprehensive coverage. Let’s go through these two.

Compulsory Third-Party Liability Insurance (CTPL)

If you purchase a new or used motorbike in Thailand, you will be required to register it in your name at the nearest Department of Land Transport office. As part of this process, you will also be required to purchase the compulsory motorcycle insurance known as Compulsory Third-Party Liability Insurance (CTPL). The locals often call this ‘Por Ror Bor’. It is illegal to ride a motorcycle in Thailand without the basic coverage of a CTPL, and you could be charged with a penalty of 10,000 baht if you’re caught without it.

This motorcycle insurance premium will cost you between 160 to 700 Thai baht depending on your bike’s engine capacity. Because it’s very cheap, the CTPL will only provide you with the most basic insurance coverage that includes your medical expenses and third-party liability for bodily injury that may be caused to others. You can make your claims directly at a partner hospital or by submitting your medical receipt to your insurance provider.

This medical coverage is limited if you are found to have caused the accident. For example, if the crash is your fault, your coverage limit is 30,000 baht. If it’s not your fault, your coverage amount could be up to 80,000 baht for medical expenses, and 500,000 baht in case of permanent disability or death.

Since this compulsory motorcycle insurance doesn’t cover any damages caused to a vehicle, many bikers will also purchase additional private insurance for more comprehensive insurance coverage.

Private Insurance

This is a form of fully voluntary motorcycle insurance in Thailand, but many bikers do get it since it allows them to repair any property damage they receive or cause as a result of motorcycle accidents. Let’s first look at the types of coverage that can be included in a private motorbike insurance plan.

One-Party Accidents

This is a type of motorbike insurance coverage for accidents where there is no third party involved. If you lose control of your bike and hit a tree, a stray animal on the road, or any other structure on the side of the road, this will count as a one-party accident. Depending on your motorcycle insurance plan, you may be required to pay a small fee called an ‘excess’ to make your claim for these accidents.

Collision Coverage

Collision coverage is what allows you to claim compensation for repairing your motorbike if it’s involved in a crash with another vehicle. If you caused the accident, you will most often be required to pay the excess fee. If the damage is so severe that your motorcycle is beyond repair, you can claim up to 70% to 100% of your motorcycle insurance coverage limit.

More expensive motorbike insurance premium plans will enable you to repair your bike at an authorized garage. For example, if you’re riding a Honda, it will be sent to the official Honda garage where you can get it fixed by certified mechanics who will be using genuine parts. Cheaper motorcycle insurance packages may send the bike to one of many independent garages which may vary in the quality of service they provide. So be aware of where your insurance company will recommend as a garage.

Medical Expenses

Every type of vehicle insurance in Thailand including the earlier mentioned compulsory motorcycle insurance package provides medical coverage. Furthermore, your health or family insurance packages can also cover medical expenses if you’re not riding a motorcycle but are involved in an accident.

Theft Protection

This coverage will allow you to claim compensation in the event your motorbike is stolen. However, keep in mind that you should act responsibly and take all necessary precautions to keep your motorcycle safe. Forgetting to lock your motorcycle or leaving it parked in an unsafe area will get your claim rejected.

Fire/Flood

Similar to a stolen vehicle, you will be able to claim damages if you were not responsible for setting fire or intentionally driving through a flooded area. You will be under the coverage if you parked in a safe area that suddenly gets flooded from a natural disaster without a warning.

Third-Party Property Damage

While a collision coverage policy will allow you to make claims to fix your bike, any property damage that is caused to a third party will be covered under this. Some of the cheaper motorcycle insurance plans will only include third-party liability. This means you don’t have to worry about paying compensation for property damages to others, although you will have to repair your bike.

Third-Party Bodily Injury

Third-party liability for bodily injury is included in both private and compulsory motorcycle insurance in Thailand. Even if you’re a pedestrian that is hit by a motorcycle while you’re out walking, you will be compensated for any bodily injury you sustain through that bike driver’s CTPL.

Exclusions in Your Motorbike Insurance Policy

Motorcycle insurance in Thailand will only allow you to make claims as long as you’ve been driving safely and responsibly. If you avoid the following exclusions, you will most likely be able to receive your compensation without any issues when you get into an accident.

Driving without a Valid Driver’s License

This is a no-brainer. You should not be driving any sort of vehicle without carrying a valid driver’s license. If your license is expired or wishes to learn how to get a new one, read How To Get A Motorcycle License In Thailand For Foreigners.

Drunk Driving

Driving under the influence of substances like alcohol could get you fined by the police or even imprisoned under Thai law. A drunk driver has a blood alcohol concentration level of over 50mg. Since this is illegal, drunk driving will also get your claims rejected.

Unauthorized Driver

Some bike insurance plans will allow you to specify an authorized driver to get your insurance premium lowered. However, this won’t cover accidents if a different or unauthorized driver is found to have been driving your bike.

Incorrect Purpose

Your claims can also get rejected if you got into an accident while using your bike incorrectly. Carrying more than what the bike can safely handle, or transporting heavy goods are examples of incorrect-purpose situations.

Leaving the Scene of Motorcycle Accidents

Leaving the scene of an accident that you caused is a crime in Thailand. You will be arrested and will need to appear before a court if you attempt such a thing. And naturally, your damages will not be covered in this case.

Damage During War/Protest

Motorcycle insurance in Thailand does not cover damages caused by war or protest. If you’re living in a risky area, it is your responsibility to keep your bike safe from harm.

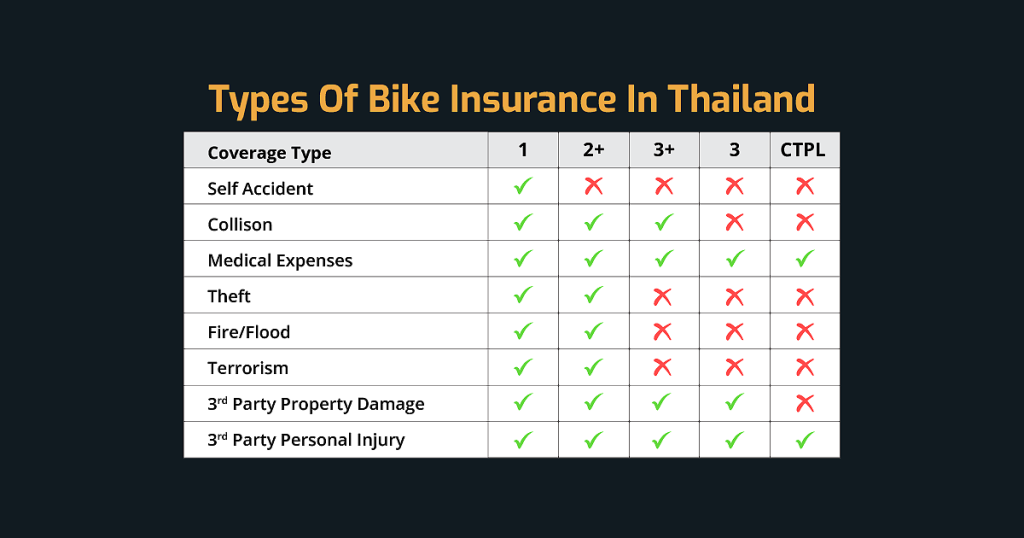

Types of Motorbike Insurance in Thailand

Bike insurance plans in Thailand will come in four different types. The best motorbike insurance package will be the most comprehensive and include most of the types of coverage we mentioned so far. It will also be the most expensive.

Type 1

Type 1 bike insurance is the most comprehensive and will keep you covered from most major accidents involved on the road. Type 1 class insurance is also the most expensive, and is the only plan that includes one-party accidents. It has everything else including collision coverage, medical expenses, theft, fire/flood, and full third-party coverage for property and bodily injury.

You can usually get Type 1 coverage for bikes that are less than five years old. For older motor vehicles, you might still be able to get Type 1 if there’s a good record for the vehicle without a history of getting into major accidents. Finally, Type 1 will also send your bike to be repaired at official garages, ensuring a high-quality service.

Type 2+

This is the second most expensive and covers everything in Type 1, except one-party accidents. While you won’t have a choice of sending your bike to be repaired at an official garage, you will get good coverage for a much more affordable premium.

Type 3+

Type 3+ will have everything in Type 2+ but will not include coverage for theft, fire, and flood damages. However, if you’re careful about the safety of your bike when it’s parked, it’s still a great choice since it covers most of the situations where your bike can get damaged or cause damage to third parties while driving it.

Type 3

This is a very basic bike insurance package that covers your medical bills, and third-party liability for property damages and bodily injury. You’ll have to pay out of your pocket to fix any damages to your bike. For a full comparison of these various insurance types, refer to the table below.

Things to Know When Buying Motorbike Insurance in Thailand

Now that you’re familiar with both mandatory insurance and voluntary motorcycle insurance packages, let’s look at a few other things you need to keep in mind when purchasing your plan.

Theft Protection Insurance Is Highly Recommended

Getting a plan that includes theft protection is highly recommended since many gangs in Thailand are involved in stealing motorbikes. In the event your bike is stolen, you will have to report it to the police and your insurance company who will attempt to locate your vehicle. It would take 30 days for your claim to be processed. You will be compensated after transferring ownership of the bike to your insurance company.

Theft protection for new bikes will have a limit of 50,000 baht and a premium between 1,000 and 2,000 baht. For bikes older than four years, the limit will be between 6,000 and 10,000 baht with a premium of around 500 baht.

Big Bike Insurance

Big bike insurance is for motorbikes that have engines over 250ccs. Type 1, 2+, and 3+ are available for big bikes and are usually more expensive than regular bike insurance premiums. In fact, a Type 1 big bike insurance premium will go up to about 15,000 baht which is what you would normally pay for car insurance.

These plans might offer lower coverage as well since there’s a higher risk of accidents with racing-type motorbikes and the spare parts needed to repair these vehicles are costly as well. Another thing to keep in mind is that the excess fee may apply even if you didn’t cause the accident, and can go up to 5,000 baht on average.

Big bikes are fun if you’re an experienced motorhead but if you’re planning on leisurely driving around Phuket or some other picturesque part of Thailand, you’re better off on a regular bike or even a scooter.

Riding without Motorcycle Insurance

Some people might be tempted to drive bikes in Thailand without getting the most basic insurance coverage. However, a quick look at the road accident statistics should convince you that it’s dangerous to attempt this. The Thailand Road Safety Situation Survey conducted by the Thailand Health Promotion Foundation and road-safety watch teams in 2018 found that nearly 70% of fatal crashes involved motorbikes.

Accidents can happen and you will need good insurance coverage to pay your medical bills which can be very expensive if you’re admitted to a hospital for many days or undergo serious surgery. So if you’re planning on driving around on a motorbike in Thailand, make sure to get insurance.

Need a Car for Driving around Thailand?

If you’re traveling with a small group of people, they’re not going to fit into your bike. Instead of getting your bike accident claim rejected, you could consider purchasing a used car that can seat everyone comfortably. Used cars can be purchased at great bargain prices in Thailand from a variety of places.

If you need information on common terms that are included in your car insurance plan like ‘excess’, ‘deductibles’, and ‘no claim bonus’ or you need help in choosing a trusted insurance company, you can read A Guide To Buying Car Insurance In Thailand which covers all of these topics and more.

Need a Local Guide in Phuket?

If you’re wondering where to go after getting your motorbike or car, then you’re going to need the help of a trusty local guide. We have traveled everywhere around the sunny island of Phuket. We know the best places to eat, stay, immerse yourself in the local culture, and go sightseeing. So, check out our blog for the best eateries, activities, and locations to visit during your stay in Phuket.

FAQs

Yes. You will need to purchase Compulsory Third-Party Liability (CTPL) insurance, also known as ‘Por Ror Bor’ to legally drive a motorcycle or car in Thailand. This provides medical and third-party coverage for bodily injury only. You will need to purchase private motorbike insurance to get better coverage.

The Compulsory Third-Party Liability (CTPL) insurance will cost you less than 1,000 Thai baht. Other private motorcycle insurance policies with better coverage will be more expensive